ROUTING NUMBER: 307070050

Rest Confident, Your Money is Safe and Secure at Kirtland Credit Union, a message from our President & CEO. Learn More

Mobile Check Deposit is Temporarily Unavailable. We apologize for the inconvenience.

All Kirtland CU branches and locations will be closed on Saturday, July 4 in observance of Independence Day.

If you have been financially impacted by the wildfires in Arizona, Colorado, and New Mexico, we’re ready to work with you on personalized solutions.

Contact us today at (800) 880-5328 to learn how we can help.

If you may experience financial hardship related to the government shutdown, we’re here to help. Contact us at 1.800.880.5328 for assistance, and click here to see how we are standing with you.

If you are experiencing financial hardship related to the government shutdown, we’re here to help. Click here to see how we are standing with you.

Use caution if you receive a call, email, or text message that appears to be from Kirtland Credit Union. Don’t click on links or call phone numbers in unsolicited messages. Remember: We will NEVER ask for your online banking access codes, credentials or for you to transfer money.

Chat Temporarily Unavailable: We’re currently experiencing issues with our chat service in Digital Banking. For immediate assistance, please call us or visit your nearest branch. We apologize for the inconvenience.

ROUTING NUMBER: 307070050

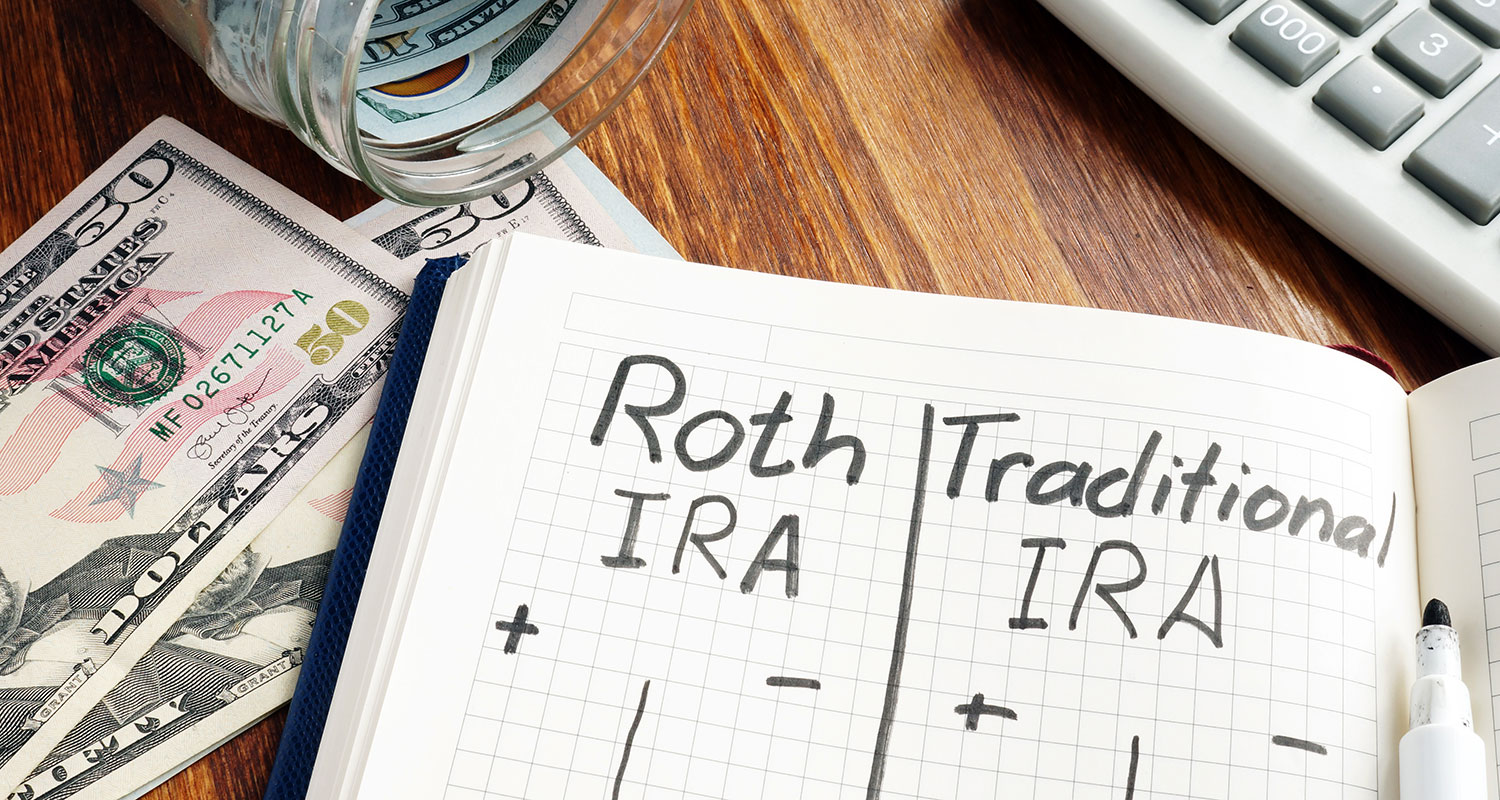

Many IRA and retirement plan limits are indexed for inflation each year. While some of the limits remain unchanged for 2021, other key numbers have increased.

The maximum amount you can contribute to a traditional IRA or a Roth IRA in 2021 is $6,000 (or 100% of your earned income, if less), unchanged from 2020. The maximum catch-up contribution for those age 50 or older remains $1,000. You can contribute to both a traditional IRA and a Roth IRA in 2021, but your total contributions cannot exceed these annual limits.

If you (or if you’re married, both you and your spouse) are not covered by an employer retirement plan, your contributions to a traditional IRA are generally fully tax deductible. If you’re married, filing jointly, and you’re not covered by an employer plan but your spouse is, your deduction is limited if your modified adjusted gross income (MAGI) is between $198,000 and $208,000 (up from $196,000 and $206,000 in 2020), and eliminated if your MAGI is $208,000 or more (up from $206,000 in 2020).

For those who are covered by an employer plan, deductibility depends on your income and filing status.

| If your 2021 federal income tax filing status is: | Your IRA deduction is limited if your MAGI is between: | Your deduction is eliminated if your MAGI is: |

|---|---|---|

| Single or head of household | $66,000 and $76,000 | $76,000 or more |

| Married filing jointly or qualifying widow(er) | $105,000 and $125,000 (combined) | $125,000 or more (combined) |

| Married filing separately | $0 and $10,000 | $10,000 or more |

If your filing status is single or head of household, you can fully deduct your IRA contribution up to $6,000 ($7,000 if you are age 50 or older) in 2021 if your MAGI is $66,000 or less (up from $65,000 in 2020). If you’re married and filing a joint return, you can fully deduct up to $6,000 ($7,000 if you are age 50 or older) if your MAGI is $105,000 or less (up from $104,000 in 2020).

The income limits for determining how much you can contribute to a Roth IRA have also increased.

| If your 2021 federal income tax filing status is: | Your Roth IRA contribution is limited if your MAGI is: | You cannot contribute to a Roth IRA if your MAGI is: |

|---|---|---|

| Single or head of household | More than $125,000 but less than $140,000 | $140,000 or more |

| Married filing jointly or qualifying widow(er) | More than $198,000 but less than $208,000 (combined) | $208,000 or more (combined) |

| Married filing separately | More than $0 but less than $10,000 | $10,000 or more |

If your filing status is single or head of household, you can contribute the full $6,000 ($7,000 if you are age 50 or older) to a Roth IRA if your MAGI is $125,000 or less (up from $124,000 in 2020). And if you’re married and filing a joint return, you can make a full contribution if your MAGI is $198,000 or less (up from $196,000 in 2020). Again, contributions can’t exceed 100% of your earned income.

Most of the significant employer retirement plan limits for 2021 remain unchanged from 2020. The

maximum amount you can contribute (your “elective deferrals”) to a 401(k) plan remains $19,500 in 2021. This limit also applies to 403(b) and 457(b) plans, as well as the Federal Thrift Plan. If you’re age 50 or older, you can also make catch-up contributions of up to $6,500 to these plans in 2021. [Special catch-up limits apply to certain participants in 403(b) and 457(b) plans.]

The amount you can contribute to a SIMPLE IRA or SIMPLE 401(k) remains $13,500 in 2021, and the catch-up limit for those age 50 or older remains $3,000.

| Plan Type: | Annual Dollar Limit: | Catch-Up Limit: |

|---|---|---|

| 401(k), 403(b), governmental 457(b), Federal Thrift Plan | $19,500 | $6,500 |

| SIMPLE plans | $13,500 | $3,000 |

Note: Contributions can’t exceed 100% of your income.

If you participate in more than one retirement plan, your total elective deferrals can’t exceed the annual limit ($19,500 in 2021 plus any applicable catch-up contributions). Deferrals to 401(k) plans, 403(b) plans, and SIMPLE plans are included in this aggregate limit, but deferrals to Section 457(b) plans are not. For example, if you participate in both a 403(b) plan and a 457(b) plan, you can defer the full dollar limit to each plan — a total of $39,000 in 2021 (plus any catch-up contributions).

The maximum amount that can be allocated to your account in a defined contribution plan [for example, a 401(k) plan or profit-sharing plan] in 2021 is $58,000 (up from $57,000 in 2020) plus age 50 or older catch-up contributions. This includes both your contributions and your employer’s contributions. Special rules apply if your employer sponsors more than one retirement plan.

Finally, the maximum amount of compensation that can be taken into account in determining benefits for most plans in 2021 is $290,000 (up from $285,000 in 2020), and the dollar threshold for determining highly compensated employees (when 2021 is the look-back year) remains $130,000 (unchanged from 2020).

How will IRA and retirement plan limits affect your plans? Kirtland Financial Services can help you navigate these rules.

If you have access issues, CONTACT KIRTLAND FINANCIAL SERVICES.

Save 0.50% off our already low auto refinance rates and enjoy 60 days without payments when you apply before May 31, 2026.