Rest Confident, Your Money is Safe and Secure at Kirtland Credit Union, a message from our President & CEO. Learn More

Mobile Check Deposit is Temporarily Unavailable. We apologize for the inconvenience.

All Kirtland CU branches and locations will be closed on Friday, June 19 in observance of Juneteenth.

If you may experience financial hardship related to the government shutdown, we’re here to help. Contact us at 1.800.880.5328 for assistance, and click here to see how we are standing with you.

If you are experiencing financial hardship related to the government shutdown, we’re here to help. Click here to see how we are standing with you.

Use caution if you receive a call, email, or text message that appears to be from Kirtland Credit Union. Don’t click on links or call phone numbers in unsolicited messages. Remember: We will NEVER ask for your online banking access codes, credentials or for you to transfer money.

Chat Temporarily Unavailable: We’re currently experiencing issues with our chat service in Digital Banking. For immediate assistance, please call us or visit your nearest branch. We apologize for the inconvenience.

ROUTING NUMBER: 307070050

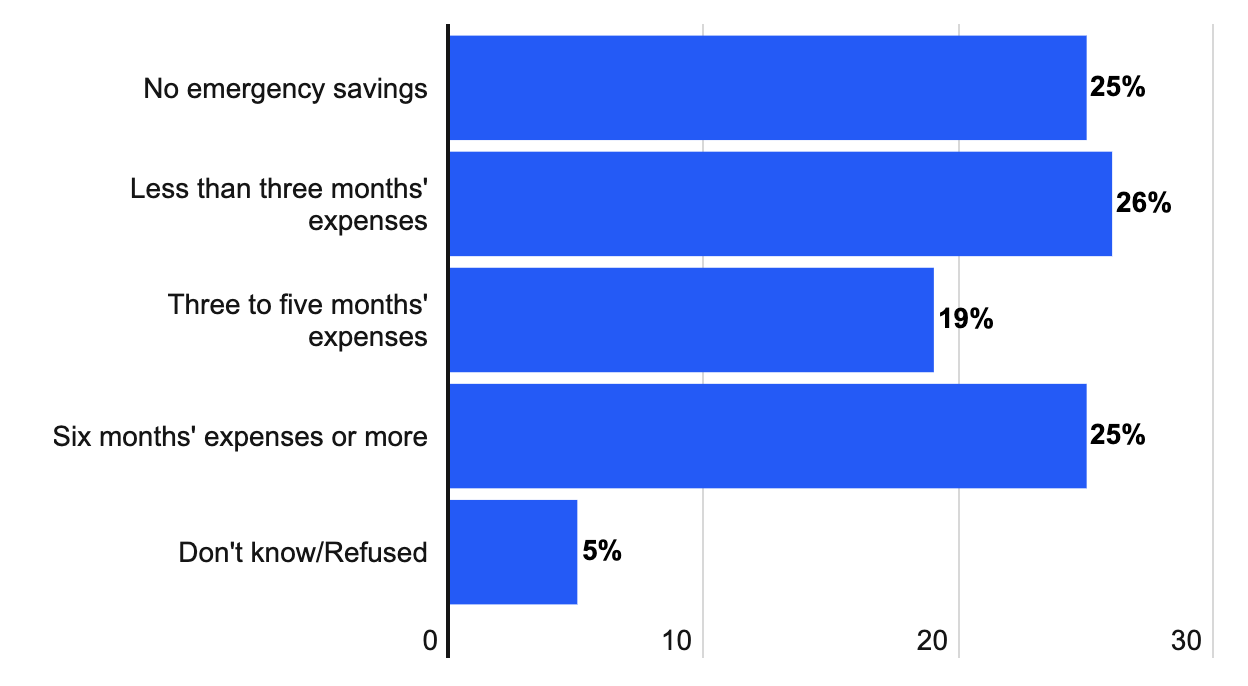

Do you have an emergency fund? If you’re like many Americans, the answer is probably no. In fact, more than half of Americans don’t have enough savings to cover three months of expenses, according to a July 2021 Bankrate.com poll. Despite multiple rounds of stimulus assistance from the federal government, just 1 in 6 say they have more emergency savings than before the pandemic started.

If you’re like most Americans, building an emergency fund should be a top priority. The good news is there are simple steps you can take today to protect yourself from whatever may come tomorrow.

Few of us anticipate having a costly crisis—but they’re so commonplace that it makes sense to be prepared. Do you have the money you would need to cover:

Nearly all of us face these situations, and credit cards and loans tend to be go-tos. But interest payments make them more expensive choices, and your particular credit situation may not be conducive to relying on these avenues. Having a savings fund ready to go can give you peace of mind during a stressful time.

A good rule-of-thumb is to save six to nine months’ worth of expenses. Factors including job stability, the ease with which you could find a similar job if you needed to, and family structure (are you the sole income-earner in your household?) all influence whether you should aim for the lower or higher end of that range.

MoneyUnder30.com has a very useful calculator for figuring a good target for your emergency fund.

Building a good emergency fund could take some time, but any amount you do save before an emergency allows you to borrow that much less.

An emergency fund is the smartest way to handle financial obstacles. If you do encounter a financial emergency and don’t have the savings to handle it, a low-rate loan or credit card are the next best option. Kirtland FCU has wide variety of savings account, credit card programs, and loan options to help you handle any expense!

Save 0.50% off our already low auto refinance rates and enjoy 60 days without payments when you apply before May 31, 2026.