ROUTING NUMBER: 307070050

Rest Confident, Your Money is Safe and Secure at Kirtland Credit Union, a message from our President & CEO. Learn More

Mobile Check Deposit is Temporarily Unavailable. We apologize for the inconvenience.

All Kirtland CU branches and locations will be closed on Friday, June 19 in observance of Juneteenth.

If you may experience financial hardship related to the government shutdown, we’re here to help. Contact us at 1.800.880.5328 for assistance, and click here to see how we are standing with you.

If you are experiencing financial hardship related to the government shutdown, we’re here to help. Click here to see how we are standing with you.

Use caution if you receive a call, email, or text message that appears to be from Kirtland Credit Union. Don’t click on links or call phone numbers in unsolicited messages. Remember: We will NEVER ask for your online banking access codes, credentials or for you to transfer money.

Chat Temporarily Unavailable: We’re currently experiencing issues with our chat service in Digital Banking. For immediate assistance, please call us or visit your nearest branch. We apologize for the inconvenience.

ROUTING NUMBER: 307070050

There’s no denying the benefits of a college education: the ability to compete in today’s job market, increased earning power, and expanded horizons. But these advantages come at a price. And yet, year after year, thousands of students graduate from college. So, how do they do it?

Many families finance a college education with help from student loans and other types of financial aid such as grants and work-study, private loans, current income, gifts from grandparents, and other creative cost-cutting measures. But savings are the cornerstone of any successful college financing plan.

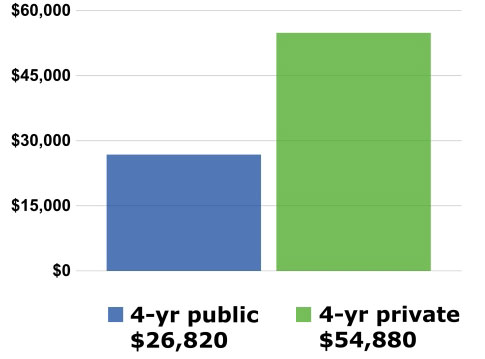

It’s important to start a college fund as soon as possible, because next to buying a home, a college education might be the biggest purchase you ever make. According to the College Board, for the 2020-2021 school year, the average cost of one year at a four-year public college for in-state students is $26,820, while the average cost for one year at a four-year private college is $54,880. Many private colleges cost substantially more. (Costs include tuition, fees, room, and board, plus a fixed sum for books, transportation, and personal expenses.)

Though no one can predict exactly what college might cost in 5, 10, or 15 years, annual price increases in the range of 3% to 5% would certainly be in keeping with historical trends.

This chart shows what future costs might be, based on the most recent cost data and an average annual college inflation rate of 5%. (Source: College Board, Trends in College Pricing and Student Aid 2020)

| Year | 4-yr public | 4-yr private |

|---|---|---|

| 2020-2021 | $26,820 | $54,880 |

| 2021-2022 | $27,920 | $56,679 |

| 2022-2023 | $29,315 | $59,513 |

| 2023-2024 | $30,781 | $62,489 |

| 2024-2025 | $32,320 | $65,613 |

| 2025-2026 | $33,936 | $68,894 |

| 2026-2027 | $35,633 | $72,338 |

| 2027-2028 | $37,414 | $75,955 |

| 2028-2029 | $39,286 | $79,753 |

| 2029-2030 | $41,250 | $83,740 |

Tip: Even though college costs are high, don’t worry about saving 100% of the total. Many families save only a portion of the projected costs — a good rule of thumb is 50% — and then use this as a “down payment” on the college tab, similar to the down payment on a home.

The more you save now, the better off you’ll likely be later. Start with whatever amount you can afford, and add to it over the years with raises, tax refunds, unexpected windfalls, and the like. If you invest regularly over time, you may be surprised at how much you can accumulate in your child’s college fund.

| Monthly Investment | 5 years | 10 years | 15 years |

|---|---|---|---|

| $100 | $6,977 | $16,388 | $29,082 |

| $300 | $20,931 | $49,164 | $87,246 |

| $500 | $34,885 | $81,940 | $145,409 |

Note: Table assumes an average after-tax return of 6%. This is a hypothetical example of mathematical principals, is used for illustrative purposes only, and does not reflect the actual performance of any investment. Fees, expenses, and taxes are not considered and would reduce the performance shown if they were included. Actual results will vary. All investing involves risk, including the possible loss of principal, and there can be no guarantee that any investing strategy will be successful.

You’re ready to start saving, but where should you put your money? It’s smart to consider tax-advantaged strategies whenever possible. Here are some options.

529 plans are one of the most popular tax-advantaged college savings options. Contributions accumulate tax deferred and withdrawals are tax free at the federal level if the money is used for qualified education expenses. States may also offer their own tax advantages. (For withdrawals not used for qualified expenses, earnings are subject to income tax and a 10% federal penalty.) 529 plans are open to anyone and lifetime contribution limits are high, typically $350,000 and up (limits vary by state). In 2021, lump sum gifting up to $75,000 is allowed ($150,000 for joint gifts) with no gift tax implications if certain requirements are met.

There are two types of 529 plans: savings plans and prepaid tuition plans. A 529 savings plan is an individual investment account similar to a 401(k) plan where you direct your contributions to one or more of the plan’s investment portfolios. Funds in the account can be used to pay tuition, fees, room and board, books, and supplies at any accredited college in the United States or abroad. Funds can also be used to pay K-12 tuition expenses, up to $10,000 per year. By contrast, the less common 529 prepaid tuition plan allows you to purchase college tuition credits at today’s prices for use in the future at a limited group of colleges that participate in the plan, typically in-state public colleges.

A Coverdell education savings account (ESA) is a tax-advantaged education savings vehicle that lets you contribute up to $2,000 per year for a beneficiary’s K-12 or college expenses. Your contributions grow tax deferred and earnings are tax free at the federal level if the money is used for qualified education expenses. You have complete control over the investments you hold in the account, but there are income restrictions on who can participate, and the $2,000 annual contribution limit isn’t likely to put much of a dent in college expenses.

A custodial account allows a minor to hold investment assets in his or her own name with an adult as custodian. All contributions to the account are irrevocable gifts to your child, and assets in the account can be used to pay for college. When your child turns 18 or 21 (depending on state law), he or she will gain control of the account. Earnings and capital gains generated by the account are taxed to your child each year under the “kiddie tax” rules. Under the kiddie tax rules, a child’s unearned income over a certain threshold ($2,200 in 2021) is taxed at parent income tax rates.

Though technically not a college savings option, some parents use Roth IRAs to save and pay for college. Contributions to a Roth IRA can be withdrawn at any time and are always tax free. For parents age 59 1/2 and older, a withdrawal of earnings is also tax free if the account has been open for at least five years. For parents younger than 59 1/2, a withdrawal of earnings — typically subject to income tax and a 10% premature distribution penalty — is spared the 10% penalty if the withdrawal is used to pay for a child’s college expenses.

Many families rely on some form of financial aid to pay for college, which may include loans, grants, scholarships, and work-study. Financial aid can be based on financial need or on merit. To determine financial need, the federal government and colleges look primarily at your family’s income, but other factors come into play, including your assets and how many children you’ll have in college at the same time.

To get an idea of how much aid your child might be eligible for at a particular college, you can use a net price calculator, which is available on every college website. The bottom line, though, is to beware of too much borrowing. Excessive student loan debt — and parent debt — can negatively affect borrowers for years. The lesson? The more you save now, the less you and your child will need to fund later.

Note: Investors should consider the investment objectives, risks, charges, and expenses associated with 529 plans before investing; specific plan information is available in each issuer’s official statement. There is the risk that investments may not perform well enough to cover college costs as anticipated. Also, before investing, consider whether your state offers any favorable state tax benefits for 529 plan participation, and whether these benefits are contingent on joining the in-state 529 plan. Other state benefits may include financial aid, scholarship funds, and protection from creditors.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional. LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

If you have access issues, CONTACT KIRTLAND FINANCIAL SERVICES.

Save 0.50% off our already low auto refinance rates and enjoy 60 days without payments when you apply before May 31, 2026.