ROUTING NUMBER: 307070050

Rest Confident, Your Money is Safe and Secure at Kirtland Credit Union, a message from our President & CEO. Learn More

Mobile Check Deposit is Temporarily Unavailable. We apologize for the inconvenience.

All Kirtland CU branches and locations will be closed on Saturday, July 4 in observance of Independence Day.

If you have been financially impacted by the wildfires in Arizona, Colorado, and New Mexico, we’re ready to work with you on personalized solutions.

Contact us today at (800) 880-5328 to learn how we can help.

If you may experience financial hardship related to the government shutdown, we’re here to help. Contact us at 1.800.880.5328 for assistance, and click here to see how we are standing with you.

If you are experiencing financial hardship related to the government shutdown, we’re here to help. Click here to see how we are standing with you.

Use caution if you receive a call, email, or text message that appears to be from Kirtland Credit Union. Don’t click on links or call phone numbers in unsolicited messages. Remember: We will NEVER ask for your online banking access codes, credentials or for you to transfer money.

Chat Temporarily Unavailable: We’re currently experiencing issues with our chat service in Digital Banking. For immediate assistance, please call us or visit your nearest branch. We apologize for the inconvenience.

ROUTING NUMBER: 307070050

Social Security benefits are a major source of retirement income for most people. Your Social Security retirement benefit is based on the number of years you’ve been working and the amount you’ve earned. When you begin taking Social Security benefits also greatly affects the size of your benefit.

When you work and pay Social Security taxes (FICA on some pay stubs), you earn Social Security credits. You can earn up to 4 credits each year. If you were born after 1928, you need 40 credits (10 years of work) to be eligible for retirement benefits.

The Social Security Administration (SSA) calculates your primary insurance amount (PIA), upon which your retirement benefit will be based, using a formula that takes into account your 35 highest earnings years. At your full retirement age, you’ll be entitled to receive that amount. This is known as your full retirement benefit. Because your retirement benefit is based on your average earnings over your working career, if you have some years of no earnings or low earnings, your benefit amount may be lower than if you had worked steadily.

Your age at the time you start receiving benefits also affects your benefit amount. Although you can retire early at age 62, the longer you wait to begin receiving your benefit (up to age 70), the more you’ll receive each month.

You can estimate your retirement benefit under current law by using the benefit calculators available on the SSA’s website, ssa.gov. You can also sign up for a my Social Security account so that you can view your online Social Security Statement. Your statement contains a detailed record of your earnings, as well as estimates of retirement, survivor, and disability benefits. If you’re not registered for an online account and are not yet receiving benefits, you’ll receive a statement in the mail every year, starting at age 60.

Your full retirement age depends on the year in which you were born. If you retire at full retirement age, you’ll receive an unreduced retirement benefit.

| If you were born in: | Your full retirement age is: |

|---|---|

| 1943-1954 | 66 |

| 1955 | 66 + 2 months |

| 1956 | 66 + 4 months |

| 1957 | 66 + 6 months |

| 1958 | 66 + 8 months |

| 1959 | 66 + 10 months |

| 1960 or later | 67 |

Note: If you were born on January 1 of any year, refer to the previous year to determine your full retirement age.

You can begin receiving Social Security benefits before your full retirement age, as early as age 62. However, if you begin receiving benefits early, your Social Security benefit will be less than if you wait until your full retirement age to begin receiving benefits. Your retirement benefit will be reduced by 5/9ths of 1 percent for every month between your retirement date and your full retirement age, up to 36 months, then by 5/12ths of 1% thereafter. This reduction is permanent — you won’t be eligible for a benefit increase once you reach full retirement age. However, even though your monthly benefit will be less, you might receive the same or more total lifetime benefits as you would have had you waited until full retirement age to start collecting benefits. That’s because even though you’ll receive less per month, you might receive benefits over a longer period of time.

For each month that you delay receiving Social Security retirement benefits past your full retirement age, your benefit will permanently increase by a certain percentage, up to the maximum age of 70. For anyone born in 1943 or later, the monthly percentage is 2/3 of 1%, so the annual percentage is 8%. So, for example, if your full retirement age is 67 and you delay receiving benefits for 3 years, your benefit at age 70 will be 24% higher than at age 67.

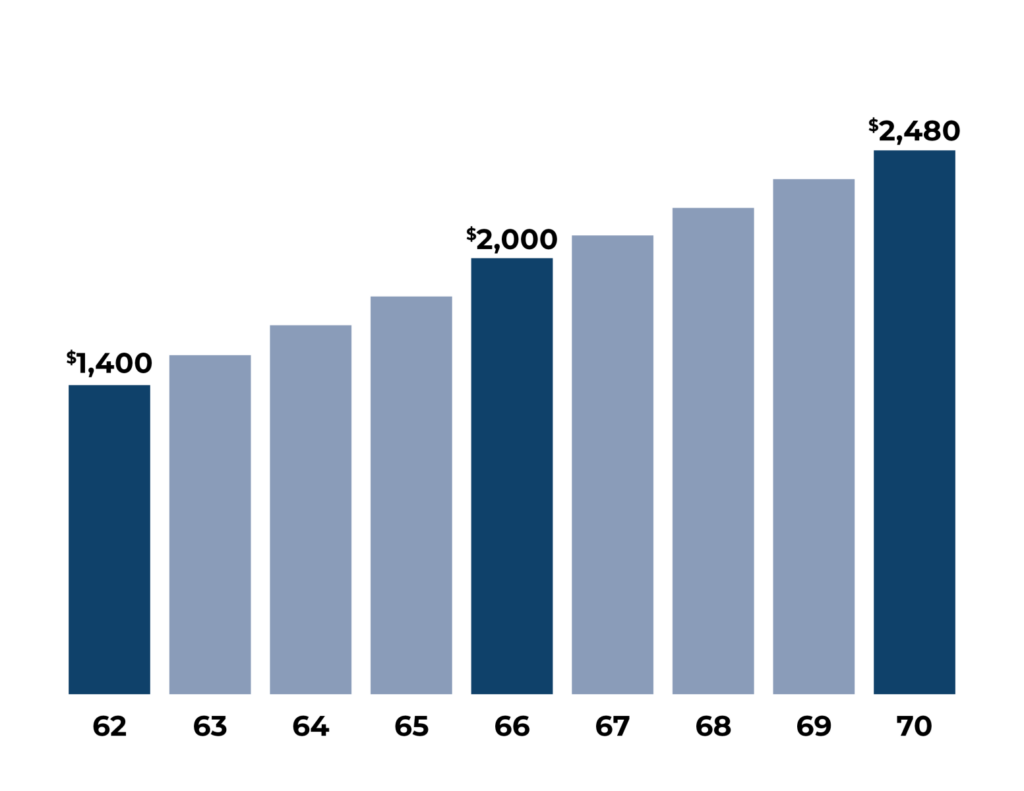

The following chart illustrates how much a monthly benefit of $2,000 taken at a full retirement age of 67 would be worth if taken earlier or later than full retirement age. For example, as this chart shows, this $2,000 benefit would be worth $1,400 if taken at age 62, and $2,480 if taken at age 70.

This hypothetical illustration is based on Social Security Administration rules. Actual results may vary.

You can work and still receive Social Security retirement benefits, but the income that you earn before you reach full retirement age may temporarily affect your benefit. Here’s how:

Once you reach full retirement age, you can work and earn as much income as you want without reducing your Social Security retirement benefit. And keep in mind that if some of your benefits are withheld prior to your full retirement age, you’ll generally receive a higher monthly benefit at full retirement age, because after retirement age the SSA recalculates your benefit every year and gives you credit for those withheld earnings.

Even if your spouse has never worked outside your home or in a job covered by Social Security, he or she may be eligible for spousal benefits based on your Social Security earnings record. Other members of your family may also be eligible. Retirement benefits are generally paid to family members who relied on your income for financial support. If you’re receiving retirement benefits, the members of your family who may be eligible for family benefits include:

Your eligible family members will receive a monthly benefit that is as much as 50% of your benefit. However, the amount that can be paid each month to a family is limited. The total benefit that your family can receive based on your earnings record is about 150% to 180% of your full retirement benefit amount. If the total family benefit exceeds this limit, each family member’s benefit will be reduced proportionately. Your benefit won’t be affected.

For more information on retirement benefits, contact the Social Security Administration at (800) 772-1213 or visit ssa.gov.

If you have access issues, CONTACT KIRTLAND FINANCIAL SERVICES.

Save 0.50% off our already low auto refinance rates and enjoy 60 days without payments when you apply before May 31, 2026.