ROUTING NUMBER: 307070050

Rest Confident, Your Money is Safe and Secure at Kirtland Credit Union, a message from our President & CEO. Learn More

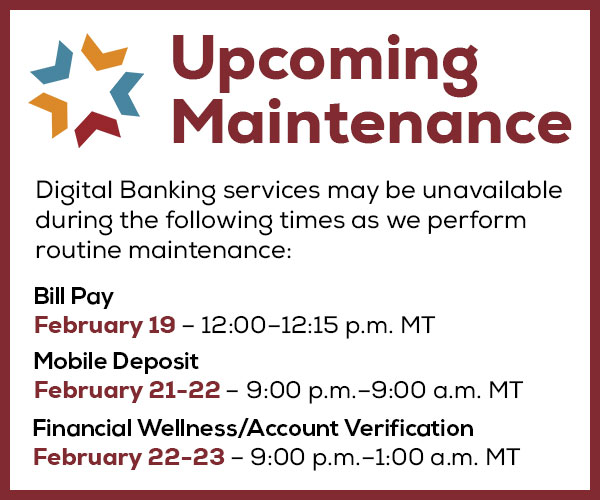

Mobile Check Deposit is Temporarily Unavailable. We apologize for the inconvenience.

All Kirtland CU branches and locations will be closed on Monday, February 16 in observance of Presidents’ Day.

Join us at our 2026 Annual Meeting at our Gibson Operations Center on Tuesday, March 24 at 5:00pm. Click here for event details.

If you may experience financial hardship related to the government shutdown, we’re here to help. Contact us at 1.800.880.5328 for assistance, and click here to see how we are standing with you.

If you are experiencing financial hardship related to the government shutdown, we’re here to help. Click here to see how we are standing with you.

Use caution if you receive a call, email, or text message that appears to be from Kirtland Credit Union. Don’t click on links or call phone numbers in unsolicited messages. Remember: We will NEVER ask for your online banking access codes, credentials or for you to transfer money.

Chat Temporarily Unavailable: We’re currently experiencing issues with our chat service in Digital Banking. For immediate assistance, please call us or visit your nearest branch. We apologize for the inconvenience.

ROUTING NUMBER: 307070050

According to Nationwide’s 8th Annual Social Security Consumer Survey, more than half of Americans express confidence that they know exactly how to optimize their Social Security benefits. However, only 6% actually understand all the factors that determine the maximum benefit someone can receive. In addition, the report highlighted additional knowledge gaps:

By mastering these lessons, you’ll immediately go to the head of the class for retirement planning—and avoid being an unfortunate statistic in some company’s future survey!

Lesson #1: Your “full retirement age” for Social Security benefits is the age at which you may first become entitled to full or unreduced retirement benefits.

Match your birth year to the full retirement ages shown below. Now, kindly memorize it!

| Birth Year | Full Retirement Age |

|---|---|

| 1955 | 66 + 2 months |

| 1956 | 66 + 4 months |

| 1957 | 66 + 6 months |

| 1958 | 66 + 8 months |

| 1959 | 66 + 10 months |

| 1960 & later | 67 |

Lesson #2: Social Security will only replace a portion of your preretirement income.

The rule of thumb is that you’ll need to replace about 75%–80% of your preretirement income. Social Security will help fund part of your income needs, generally somewhere between 25%–40% (depending on your earnings history). Your personal savings and retirement account will have to make up the difference.

Lesson #3: The longer you wait until you start taking your Social Security benefits, the more money you’ll receive.

Age 62 is the minimum age at which you can choose to begin receiving Social Security benefits. However, the math is pretty black and white: claiming earlier gives you a reduced benefit and claiming later gives you an increased benefit. For each year you postpone taking your benefit (until age 70), your monthly check will be larger. Check out the Social Security Benefits Planner (www.ssa.gov/planners) for more comprehensive information, including calculators and other resources.

Lesson #4: Social Security benefits are somewhat protected against inflation.

For 2022, the Social Security Administration is paying out a cost-of-living adjustment of 5.9%. In planning for your retirement income, it’s important to note that any cost-of-living adjustment from the Social Security Administration can vary each year and is not guaranteed. Cost-of-living adjustments are typically announced in October of each year.

This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal or investment advice. If you are seeking investment advice specific to your needs, such advice services must be obtained on your own separate from this educational material.

If you have access issues, CONTACT KIRTLAND FINANCIAL SERVICES.